Radio spectrum is the lifeblood of wireless networks. Traditional methods of doling out spectrum have somewhat hindered rather than helped maximize the availability of affordable Internet access, even if this was not the case with voice and text. Instead of seeking to aggrandize auction proceeds by creating scarcity, more flexible allocations including shared as well as traditional licensed and unlicensed assignments are required.

The proposition that expanding communications availability requires additional spectrum and shared use among service providers, as well as users, was in focus at the Dynamic Spectrum Alliance's Global Summit recently.

Horses for Courses

Allocations of unlicensed spectrum at relatively low power for local-area use have always made great sense. Even in areas with dense user populations-such as in airports, hotels or apartment blocks-unlicensed spectrum availability has, for most of us, most of the time, kept up with our increasing demands for WiFi. These places also tend to have readily-available wide-area connectivity by wire or fiber, as well as via cellular, so that Internet access is generally assured.

According to one DSA conference speaker, WiFi carries five times more data than cellular. To cheers of delight by aficionados of what this event promotes we were also told that "cellular has had the s*** kicked out of it by WiFi." Another speaker boasted that WiFi exhibits more rapid innovation with shorter times between new generations of technology than cellular.

Comparing WiFi with cellular or other wide-area wireless technologies is, however, rather like comparing apples to oranges. WiFi is largely complementary to cellular in terms of reach and other functionality which is much more extensive in cellular (e.g., at least thousands of times more coverage, high-speed handover, more numerous frequency bands, near-universal voice calling and roaming to networks in every foreign nation). With the distinct possibility that fixed-wireless access will take off in a major way, at last, with 5G including mmWave, following disappointing results or outright failure of FWA in various attempts since before the turn of the millennium, WiFi and cellular will become even more interdependent than they are today.

Coverage and Capacity

There are two distinct challenges in building-out any wireless network: coverage and capacity.

Cellular network technologies were initially oriented towards wide-area coverage outdoors based on where people live, work, play and along the transit corridors between these places. Coverage elsewhere, including indoors and in sparsely-populated areas, was deficient. This has significantly improved over the decades but remains patchy. For example, I had no cellular service in a second-floor conference room of a hotel adjacent to London's Wembley Arena and the national football stadium where the DSA event was held. WiFi coverage is also patchy nationwide: but gaps can be filled relatively quickly and cheaply, so long as landlords are amenable and if wide-area connectivity is available.

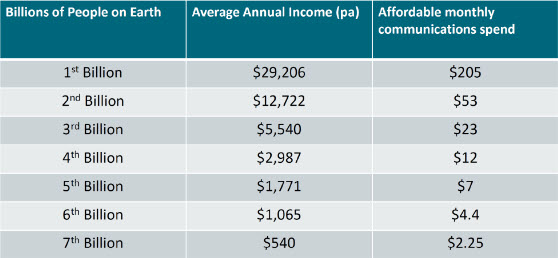

It is uneconomic to provide service in remote areas where few people live or are only occasionally, even in wealthy nations. In lower-income countries, many nationwide have gotten by with some text messaging, and voice calls for several years, but large proportions go without effective Internet access because they cannot afford to pay enough to justify the investment required. The following table estimates affordability for communications segmented by income level.

The Reality of the Affordability & Reach Challenge

Source: Presentation, at DSA 2018 Global Summit, by Jim Carlson of Carlson Wireless Technologies, based on work by Richard Thanki, University of Southampton, using UN & ITU data

The lower dollar figures for the last few billion people have been insufficient, even when subsidized by Facebook or others providing circumscribed Internet access in exchange for their data. For these people, the issue is not how many hundreds of megahertz are being wasted by licensed frequencies remaining unused in their area, it is that some suitable spectrum is deployed so that digital exclusion is prevented and affordable Internet access is provided. The objective is to make available and drive-down the cost of any Internet access at all to billions of people, and of reducing the cost per GB for the rest of us who are already connected.

Cellular capacity has been increased in proportion to the number of subscribers multiplied by the number of minutes and megabytes of data consumed. Measures to increase capacity-including deploying additional spectrum and cell splitting-have, therefore, tended to be focused on urban areas where there are lots of people. This formula tends to be economically viable in developing as well as developed nations.

Use It or Share It

Elsewhere, many people are underserved or unserved by any operator, despite the existence of unused spectrum and willingness of some would-be service providers, communities, and end-users to invest in and pay for networks and services. In many cases, the economics may be at best marginal and uninteresting to national players with higher priorities and bigger fish to fry elsewhere.

While cellular spectrum is generally licensed on a national basis, or across large areas including both densely- and sparsely-populated areas, its deployment is heavily skewed towards urban areas with much of it typically lying fallow elsewhere. Operators are forced to focus on where profits are highest to provide a return on their major investments including spectrum fees. Speakers at the DSA conference including Preston Marshall from Google criticized conventional licensed-spectrum allocation methods.

I have also advocated service obligations instead of simply maximizing spectrum-auction proceeds over many years in various articles. For example, in another trade publication, in 2010, I wrote "politicians can earn popular credit with fund-raising schemes such as auctioning spectrum to the highest bidder. And, they can also curry favor from the electorate-particularly in rural communities-by giving some of the money back (possibly to precisely the same players) with grants and subsidies for the worthy cause of building near-universal broadband access. They can even claim credit for making work for public employees to administer the scheme.

I suggest it would be better to let the operating companies keep more of their money in return for exacting network rollout and service obligations with the new spectrum. Auction prices would be lower if such obligations were imposed on spectrum owners. Tax reductions can always be spent more rapidly than grant funding and a whole layer of bureaucracy in allocating funds could be eliminated."

However, as I have also previously warned, simply giving away licensed spectrum in lotteries or discounting prices to certain categories of purchasers (e.g., ethnic groups or challenger operators) has tended to benefit those recipients rather than consumers. Spectrum tends to end up in the same hands of the leading operators eventually, with intermediate owners making windfall gains as they sell-on their spectrum or companies.

Increasing shared use of spectrum, including Citizens Band Radio Service (CBRS), Licensed Shared Access (LSA) and TV White Spaces (TVWS) enables secondary users such as new-entrants including communities to provide broadband Internet services. Secondary users access spectrum cheaply and without the administrative burden of acquiring it on a conventional licensed basis. National database services supporting these new wireless technologies enable idle frequencies to be reallocated from primary users to others on a temporary or semi-permanent basis. These technologies can provide wide-area communications on a mobile or fixed wireless access basis. In the latter case, local-area connectivity can be provided by wire or WiFi.

It Takes All Kinds to Make a Wireless World

There is still need for additional licensed and unlicensed spectrum. Only exclusive availability of licensed spectrum can ensure communications availability and quality of service and on a wide-area basis where contention for frequencies is greatest. For example, some exclusive use is essential in Ultra-Reliable and Low-Latency Communications (URLLC) which is one of upcoming 5G's three dimensions for performance improvement. Unlicensed spectrum for WiFi, now also for LTE's Licensed Assisted Access (LAA) and soon with 5G, will continue to provide local-area coverage with extended capacity on an opportunistic and best efforts basis. LAA also maintains an "anchor" in licensed spectrum.

Although, together, these opposite spectrum allocation methods have provided coverage and adequate capacity for most of us, this approach alone has deprived some users from benefitting from unused spectrum for coverage in marginally economic areas and for capacity in areas where end-user traffic demand is high. In sparsely-populated areas of developed countries and more widely in low-income countries, large amounts of spectrum are unused by licensees while would-be operators are blocked from accessing it. In these places and even in densely-populated parts of developed countries, spectrum licensees are motivated to hoard the spectrum they have paid for until they choose to use it, if ever, and to prevent others from doing so in the meantime.

Spectrum-sharing will lower barriers to entry for service providers, reduce their break-even points and lower the cost of broadband Internet access to end users. The biggest opportunity in spectrum sharing it to bridge the digital divide by connecting to people where while most spectrum is lying unused, and where other network costs and consumer price sensitivity are highest due to remote locations, low population densities, and low incomes. Elsewhere, it provides the opportunity for challengers to stir things up with a bit more competition.